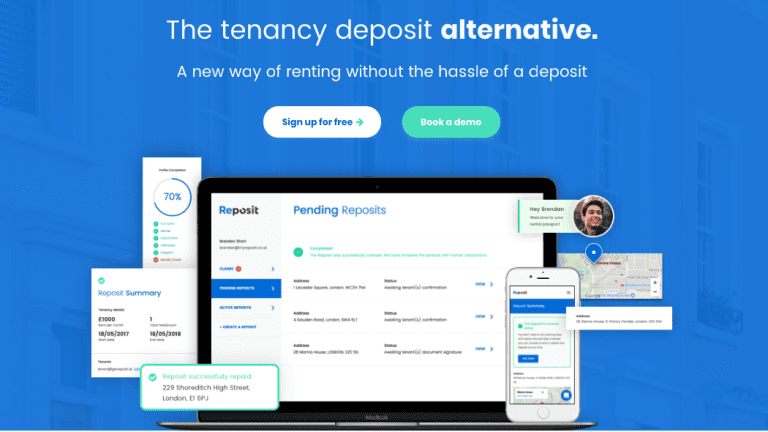

Reposit, the company changing the way landlords, agents and tenants handle deposits, has announced its latest partnership with property management company Way of Life, providing all customers with an alternative to the tenancy deposit schemes. The InsurTech firm operating in the PropTech space, has also unveiled an extension of its cover from six to eight weeks, covering all bases from rent arrears to cleaning and damages costs. Founded in 2015, Reposit is the creator of the growing deposit replacement sector in residential lettings, providing customers with an alternative to the standard tenancy deposit. Reposit eases cash flow problems for renters by enabling them to secure a property with just one week’s rent. Way of Life is a property management company currently managing over 550 homes in the UK, with another 300 launching this summer. Its customers enjoy a tailored service from point of enquiry, throughout their stay and until they move on to the next stage of their life. Way of Life customers are given the choice of purchasing a Reposit with just one week’s rent, plus an annual fee of £30 should they stay for more than one year in their home. Way of Life becomes a named beneficiary on the Reposit insurance policy and is protected for up to eight weeks’ rent, for anything a traditional tenancy deposit would have covered. “We want to offer an excellent level of service to our customers. Finding an alternative deposit option was always high on our agenda. After looking at the various deposit replacement offerings, we have chosen to partner up with Reposit to offer a viable option to our customers. It’s ease of integration into our services and the dedication towards compliance under FCA regulation and FSCS protection made the choice easy in the end,” said Way of Life’s Managing Director, Sowgol Zarinchang. Way of Life’s partnership with Reposit comes just before the opening of its new £37 million development in Birmingham, The Lansdowne, which comprises 206 apartments and more than 10,000 sq. ft of shared social spaces including a lounge with big-screen entertainment facilities, a quiet room, a broadband-equipped workspace, a fitness studio and a rentable private party room and kitchen. All customers are invited to choose a Reposit or traditional deposit when signing up. Reposit is also today announcing that it has increased its length of cover to eight weeks, the longest complete cover in the industry. A number unmatched by traditional deposits as government legislation for rent under £50,000 per year is capped at five weeks and six weeks for rent over £50,000. According to recent figures published by the Tenancy Deposit Scheme, the average rental deposit in England and Wales is £1,041, whilst in London, it is typically £1,750. Reposit’s market research data of 1,000 tenants, found that 91 percent of tenants have paid a deposit, with 49 percent claiming they borrowed from family, loans or even payday loans. For people moving between properties, they are expected to provide the deposit for the new contract before an old deposit has been released, causing further cash flow problems and added stress.