Dynamic Containment is making headlines in the field of batteries, but increasing the yield of the energy market is a much more important topic for investors.

A speeding-up UK energy change is uplifting news for battery ventures. Inexhaustible targets are rising quickly. Coal, atomic and CCGT limit is resigning.

The cold, low wind, and atomic blackouts have seen the network giving six power edge see across Winter 2020-21, with market cost signals answering appropriately. As sustainable volumes develop and firm limit resigns, there is set to be a primary expansion in these times of snugness, bringing about rising returns for adaptable resources.

UK battery returns have been out of this world across the colder time of year, principally because of high incomes from the new Dynamic Containment (DC) recurrence reaction administration.

In the present article, we take a gander at the elements set to disintegrate the DC party excitement. We likewise backtest battery gets back from wholesale & balancing markets and set out why this is a more significant story for battery financial backers.

Dynamic containment is evolving

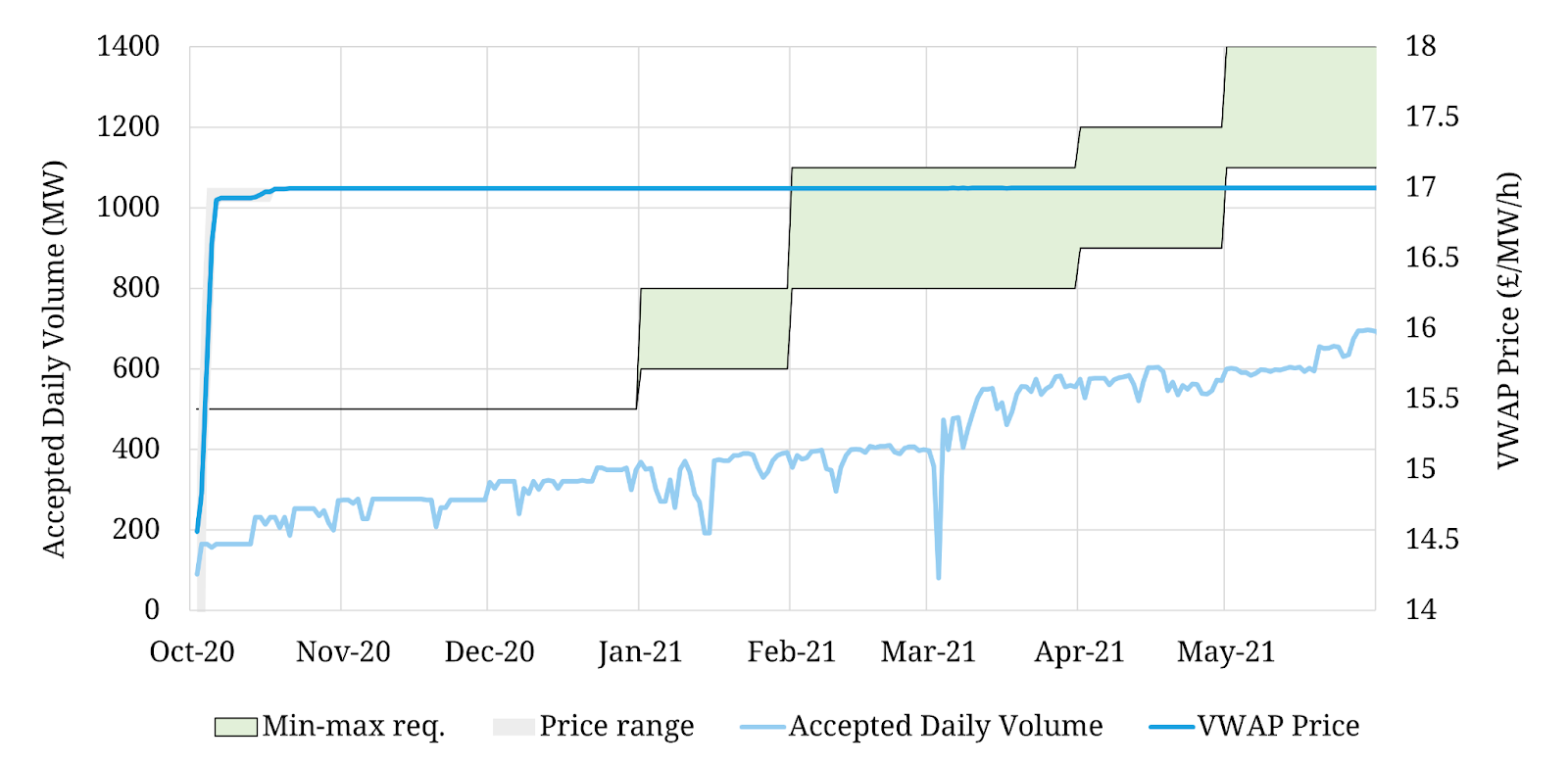

National Grid presented another DC recurrence reaction administration in Q4 2020 which has considerably expanded UK battery incomes. Graph 1 shows Grid’s interest in this assistance (concealed in green – up to 1.4GW) which as of now altogether surpasses the battery limit ready to supply DC (the light blue line – around 0.7GW).

Graph 1: Pricing & Volume of Dynamic Containment

Source: National Grid ESO

What might be compared to 150 £/kW/year in annualized income terms? DC incomes at these levels are altogether higher than both:

- incomes expected to procure a feasible profit from battery speculation;

- incomes accessible in wholesale & balancing markets.

Therefore it right now pays for battery administrators to concentrate on DC versus energy market choices, despite the fact that we are beginning to see more cross-market streamlining.

Prior to dashing out to put resources into batteries to gather these profits, there are a few changes coming to the DC market that mean a lot to process. The network has hailed a bunch of DC rule acclimations to produce results from late this mid-year. These include:

- moving to acquire DC by EFA block (as of now every day)

- moving to a ‘pay as cleared’ closeout (presently ‘pay as offered’).

The point of these progressions is to boost battery administrators to offer the minimal expense of administration arrangement, better objective necessities, and lessen by and large expenses. Benchmarking battery revenue shows that the progressions will likewise reasonably drive more batteries into the energy market at night tops, which are for the most part a time of lower recurrence reaction interest, expanding cross-income stream enhancement.

The auxiliary services party is beyond midnight

Dynamic Containment is endorsing exceptionally sound battery returns in 2021. However, incomes at current levels are a transitory peculiarity. The rollout of the new battery limit in the UK is set to rapidly surpass Grid’s interest in DC administration services (which is probably going to remain somewhat steady).

At the place of immersion, premium returns in the DC market will be disintegrated away and this is probably going to happen generally rapidly. There is as of now a little more than 1 GW of battery limit on the web. Another GW will go far to depleting the DC punch bowl.

When DC immersion is reached, the evaluation of DC (and its cousin FFR) will be driven by the gamble-changed assumptions for incomes in the lot further energy market (for example discount and adjusting markets). This doesn’t imply that recurrence reaction incomes vanish out, however, they are set to be consigned to ‘side show’ status comparative with energy market returns in the income stack.

The DC party might be seething right now, however, the shrewd financial backer cash is looking past DC to the discount and adjusting incomes that drive battery venture cases. So we should investigate how energy market incomes have been advancing behind the fervor of DC.

Backtesting battery energy market incomes

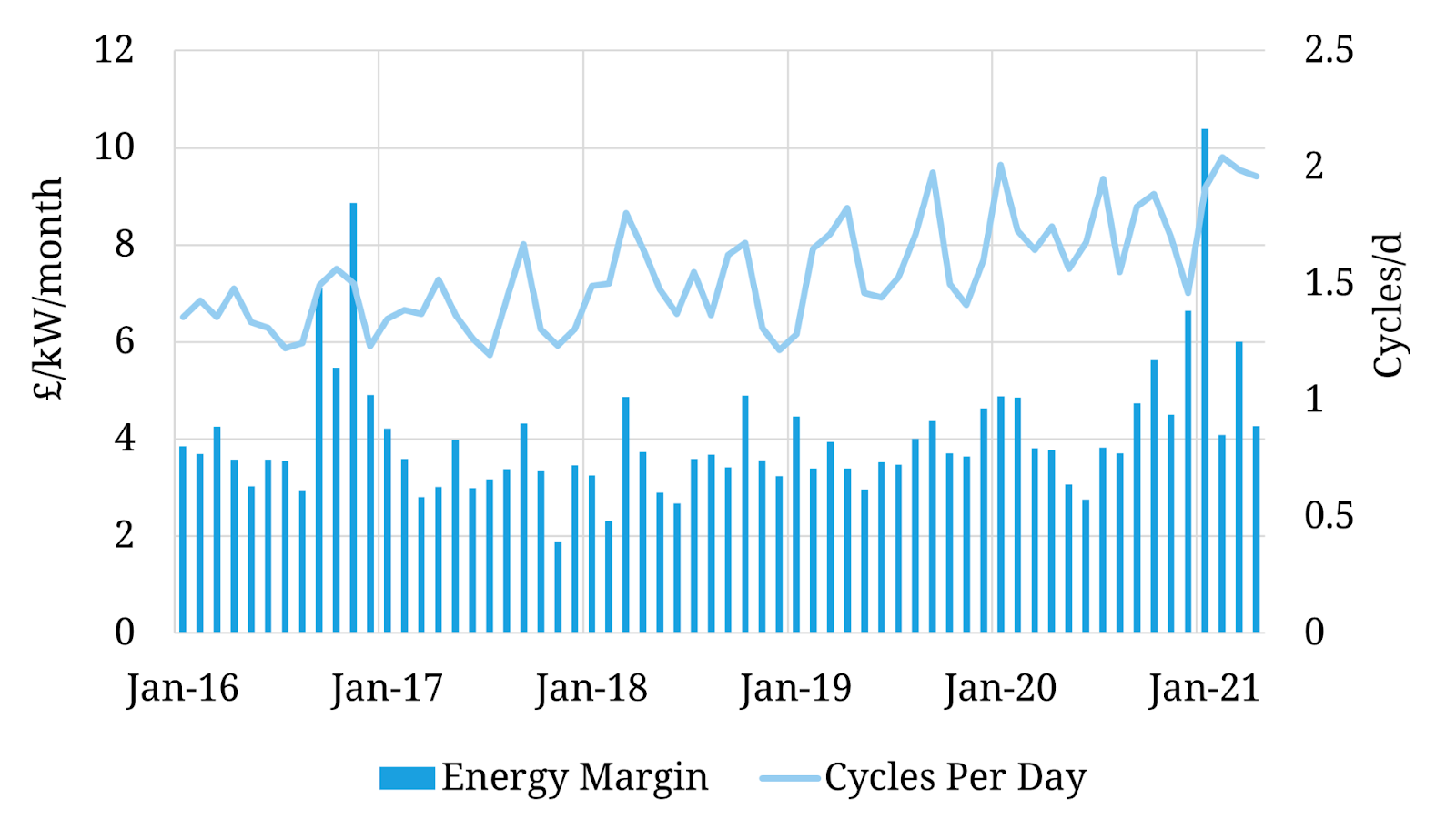

Graph 2 shows our examination of feasible battery incomes, expecting enhancement against verifiable wholesale and Balancing Mechanism (BM) costs across the most recent 5 years for a 90-minute length battery.

Graph 2: Backtested battery energy market incomes (90-minute length)

Source: Timera Energy

This examination is run utilizing Timera’s stochastic battery dispatch advancement model. This model has upheld interest in many battery projects across Europe. Its remarkable component is it reproduces the viable dynamic interaction that a merchant faces while dispatching a battery (for example catching cost vulnerability and defective foreknowledge). We know this since we work straightforwardly with a few exchanging work areas dispatching batteries.

The backtesting investigation includes improving the dispatch of the battery against authentic costs. Our methodology successively ventures through Day-Ahead, Within-Day, and BM optimization (plus the last re-advancement following BM dispatch). At each moment, choices are made in view of accessible market data (flawed premonition).

The most frequently cited authentic benchmark for high adaptable resource edges is Winter 2016-17, driven by French atomic blackouts. 2018-19 was a more troublesome period for flex resource returns in the UK, with warm and blustery circumstances and a hearty limit-hold edge.

Battery incomes rose altogether in 2020 and have been fundamentally higher across Winter 2020-21, outperforming levels of Winter 2016-17. As a benchmark, battery energy edge found the middle value of 6.8 £/kW/month in Q1 2021 (82 £/kW/year on an annualized premise).

This mirrors the fixing UK market balance (with the conclusion and retiring of coal, CCGT, and atomic plants) as well as a quickly rising infiltration of renewables. These patterns are set to characterize the development of the UK power market for a long time to come.

DC is getting battery titles in 2021, however, fundamentally expanding energy market returns is a significantly more significant story for financial backers.

Building, Design and Construction Magazine | The Choice of Industry Professionals