- The value of underlying work starting on-site during the three months to March fell 35% against the preceding three-month period to stand 46% lower than a year ago.

- Residential construction-starts slipped back 39% on the preceding three months and 51% against the previous year.

- Non-residential project-starts fell by 33% against the preceding three months to stand 42% down on a year ago.

- Civil engineering work starting on-site declined 28% against the preceding three months, 29% down against the previous year.

Glenigan, one of the construction industry’s leading insight experts, releases the April 2023 edition of its Construction Index.

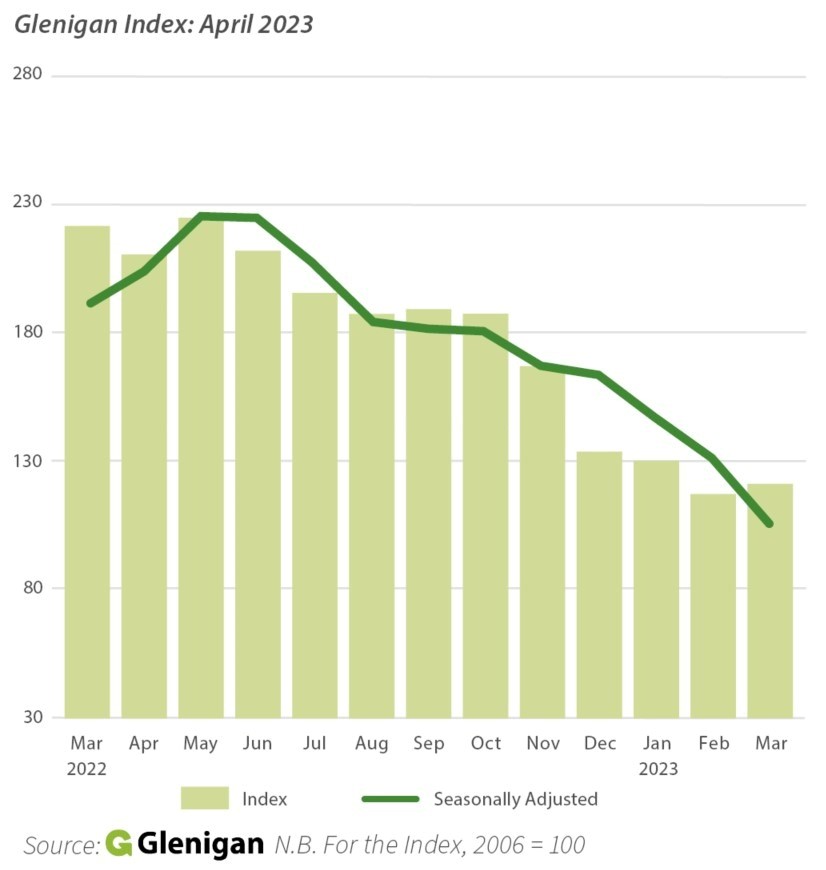

The Index focuses on the three months to the end of March 2023, covering all underlying projects, with a total value of £100m or less (unless otherwise indicated), with all figures seasonally adjusted.

It’s a report which provides a detailed and comprehensive analysis of year-on-year construction data, giving built environment professionals a unique insight into sector performance over the last 12 months.

Heading into Q.2 2023, the April Index shows construction-starts continuing to slide on a downhill trajectory. Similar to the February and March editions of the Index, project-start performance remained frustratingly slow across the sector throughout Q.1, amid eye-watering price inflation and intense economic uncertainty.

This protracted period of depression is emphasised through a massive 46% decline during the Index period, compared to last year’s figures, as climbing interest rates keep public and private investors cautious about committing to new projects.

Commenting on the findings, Glenigan’s Economic Director, Allan Willen, says, “Poor construction performance in the three months to March is disappointing but unsurprising, with a continued slowdown in project-starts reflecting the UK’s stagnant economic situation. Despite the Chancellor’s confirmation that we are not entering a recession in last month’s Budget, the UK economic outlook remains weak. Investor and consumer confidence is at a low ebb which has, inevitably, stalled private sector activity.

“Public sector starts have also disappointed, reflecting capital under-spending by a number of government departments during the last financial year. However, the Chancellor also used the Spring Statement as an opportunity to bring forward some of these underspent funds to the new financial year. This is potentially good news for those contractors specialising in critical infrastructure, where this money will likely be committed, helping to boost the industry through greater investment in mega-projects and transport upgrades throughout the rest of 2023.”

Taking a closer look at sector verticals and UK regions…

Sector Analysis – Residential

Residential construction experienced overall decline in the three months to March as starts fell 39% to stand 51% lower than a year ago.

Private housing performance was particularly weak, finishing 39% down against the preceding three months and by half compared with the previous year.

Social housing also dropped back, with work starting on site falling 41% against the previous three-month period, plummeting 52% on 2022 levels.

Sector Analysis – Non-Residential

The value of starts across non-residential sectors fell by a third (-33%) during the three months to March, finishing 42% lower than 2022 figures.

Overall performance was weak, with all verticals experiencing a decline against the preceding three-month period.

Industrial project-start performance was especially poor, with project-starts weakening 50% during Q.1 to stand 64% lower than a year ago. Retail also fared poorly, with the value of project-starts falling back 32% against the preceding three months and 48% against the previous year.

It was a similar story for offices, stumbling on a previous flurry of activity in Q4 2022. The value of underlying project-starts fell back 32% during Q.1 to stand 40% down on a year ago.

Health project-starts also slipped back abruptly, declining 36% against the preceding three months to stand 42% down on the year before.

Hotel & leisure and community & amenity also decreased 44% and 5% against the preceding three months, to stand 40% and 19% down on the previous year, respectively.

Education starts fell down 5% against the preceding three months but increased a modest 4% on 2022 levels.

Civils work starting on-site dropped 28% against the preceding three months to stand 29% down on a year ago. Infrastructure starts dropped 43% against the preceding three-month period, down 49% on the previous year’s figures.

However, in a rare bright spot amid the overall gloom, civils general decline was partly offset by utilities activity, which only declined 3% in Q.1 2023, but finished 23% up on a year ago.

Regional Analysis

Regional performance was poor, with project-starts weakening across all areas of the UK during the three months to March.

Yorkshire & the Humber suffered the heaviest fall, declining 57% during Q.1 to stand 65% down on a year ago.

It was a similar story in the South East, with the value of project-starts decreasing 48% against the preceding three months and remaining significantly down (-52%) on the previous year.

Faltering on its strong performance in recent months, project-starts in the North East experienced a sharp fall against both the preceding three months (-46%) and previous year (-41%).

London and the South West weakened against the preceding three months, falling back 28% and 24%, respectively. Both regions were down on the previous year, remaining 42% and 31% lower than a year ago.

Some areas of the UK fared even worse, including Scotland where the value of project-starts fell 48% against the preceding three months to stand 56% down on a year ago. This was also the case in the East Midlands, West Midlands, Wales, Northern Ireland, and the North West which all crashed compared to both the preceding three months and previous year.

To find out more about Glenigan and its construction intelligence services click here.

2023 sees Glenigan celebrate its 50th anniversary, commemorating half a century of delivering the highest-quality construction market intelligence. To find out more about its services and expertise click here.

Building, Design & Construction Magazine | The Choice of Industry Professionals