- Analysis of Contract Awards shows a clear rebound in construction activity in February.

- Analysts highlight potential impact of Iran conflict on future progress.

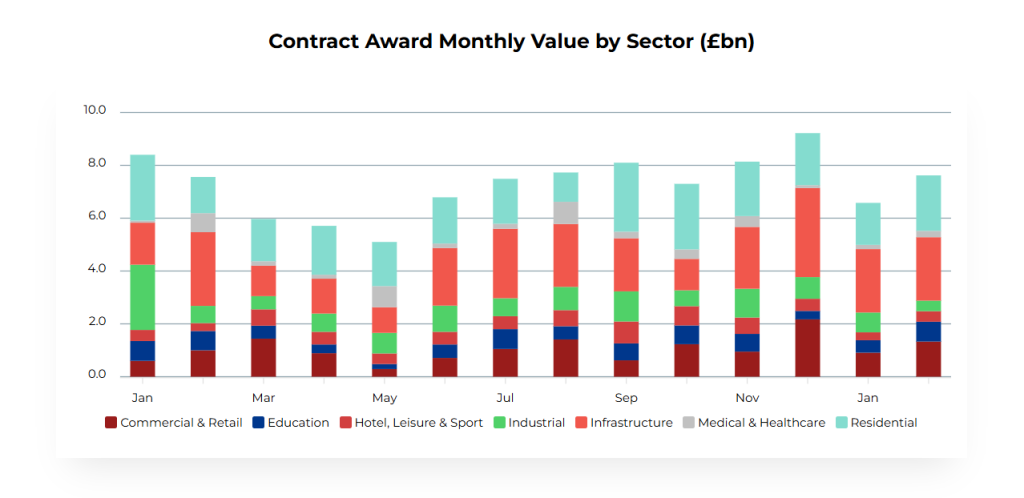

February showed a clear rebound on construction activity, with strength concentrated in Residential, Commercial, Education and major infrastructure schemes according to construction data analysts Barbour ABI. Contract Awards were up 16% month on month after a poor January with Residential rising significantly.

Commenting on the trend Barbour ABI head of business and client analytics Ed Griffiths said:

“The market is increasingly driven by large‑scale regeneration, data‑centre demand, and energy‑transition projects such as HVDC cabling, all of which continue to attract investment despite wider economic uncertainty.

Growth in residential awards reflects pent‑up demand for student accommodation and urban living, while commercial recovery is being supported by logistics‑led developments and digital infrastructure.”

Residential contract award value increased 32% on January to £2.1bn after an easing. The sector Q1 average now sits just above the average for the same period last year. The largest project in the sector was the replacement 2,330 bed student accommodation, Cambridge Halls in Manchester.

The North West, bolstered by large Residential projects and Birkenhead regeneration, saw a 158% increase to £1.16bn after a disappointing start to the year.

Meanwhile approvals ticked down 9% to £10.1bn but momentum remains strong with several large residential and mixed‑use schemes achieving consent. The continuing throughput of schemes above £100m demonstrates planning authorities’ commitment to progressing strategic housing and urban regeneration pipelines.

Clouds on the horizon

However, looking ahead Griffiths sounded a note of caution.

“In many ways it’s good news this month but across the sector, contractors still face tight margins, supply‑chain volatility and prolonged planning timelines, which are slowing momentum in some regions. Meanwhile the OBR downgraded GDP growth forecasts for the recent spring statement from 1.4% to 1.1%. Although they were more optimistic about 2027 this did not take into account the potential impact of the US-Israel strike on Iran.

“This kind of event reminds us that much of the current uncertainty in the UK construction market lies outside domestic policy control, which adds a further restraint on investment. A spike in oil and gas prices as a result of the current conflict would greatly exacerbate the viability issues that plague the market and halt any progress on delivery.”

Building, Design & Construction Magazine | The Choice of Industry Professionals