Glenigan’s April Construction Index uncovers an industry struggling to cushion the blows from ongoing international conflict and a persistently weak economy.

- Work starting on-site declined by 17% compared to Q4, remaining 18% below 2025 levels.

- Residential construction starts dropped by 13% during the Index period and fell by 30% against 2025 figures.

- Non-residential project-starts dipped by 5% against 2025 levels, falling by 15% against the preceding three months.

- Civils work starting on-site plummeted by 37% against Q4 and nosediving 34% against the previous year.

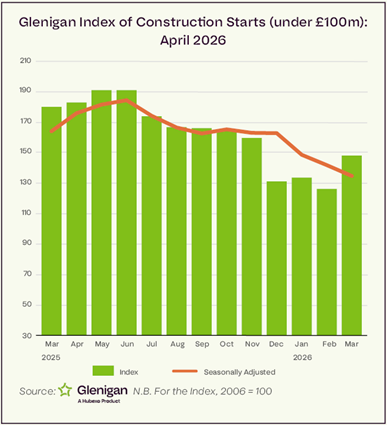

Glenigan releases the April 2026 edition of its Construction Index.

The Index focuses on the three months to the end of March 2026, covering all underlying projects, with a total value of £100m or less (unless otherwise indicated), with all figures seasonally adjusted.

It’s a report which provides a detailed and comprehensive analysis of year-on-year construction data, giving built environment professionals a unique insight into sector performance over the last 12 months.

April’s Index highlights the serious challenges facing the UK construction sector, which seem to be relentless. The industry remains in the tight grip of decline which, if not terminal, is having a deeply damaging effect, pushing its resilience to a breaking point.

A phenomenal series of socioeconomic events and foreign policy decisions have resulted in a severely disrupted supply chain and unprecedented market volatility. It all comes as yet another hammer blow falling on contractors and subcontractors alike; stalling activity, flattening margins and denting profits.

The US-Israel/Iran War started at the end of February and shows no sign of coming to an end any time soon, resulting in considerable uncertainty that’s set to keep sector performance subdued. Whilst some of the negative effects are being felt in the here and now, the expected aftershock of the continued closure of the Strait of Hormuz, alongside the increasing threats posed to the Suez Canal and Red Sea, mean disruption is predicted to continue through Q2 and Q3 2026.

Amid this maelstrom, new projects commencing in the coming months are expected to be impacted. This comes after work starting on site fell once again, particularly when seasonally adjusted, dropping by 17% compared to Q4 to finish almost a fifth (-18%) below 2025 levels.

Residential construction tumbled yet again, as international conflict, persisting confusion around planning policy and a weak economy continue to hinder development. Ice-cold investors and apprehensive potential buyers are keeping their hands firmly in their pockets for the time being.

For Non-Residential, Offices remained a strong outlier, posting impressive project-start increases compared to both the previous quarter and last year. However, these impressive figures were not nearly enough to outweigh overall disappointment in these verticals, with civils tanking against both periods covered by the Index.

Commenting on the April Index, Glenigan’s Allan Wilen says, “Superficially, looks can be deceiving. A seasonal rise during the first quarter is masking a renewed weakening in project starts. All three main verticals: housing, non-residential buildings and civil engineering are considerably lower than a year ago and on the previous quarter on a seasonally adjusted basis.

He continues, “The sector is fighting on all fronts, home and abroad. Particularly, the Iran War will depress activity further near-term as private developers and house purchasers delay investment decisions due to fears of higher than anticipated interest rates, rising material costs, spiralling energy costs and stalled economic growth. It will have a knock-on effect on the non-residential verticals which, although many have ring-fenced funding, will no doubt be putting activity on hold to ensure they don’t waste budgets whilst rates spike.”

Taking a closer look at the sectors, verticals and regions…

Sector Analysis – Residential

As above, Residential experienced a particularly poor period, according to Glenigan’s figures. Project-starts declined by13% on the preceding three months and by almost a third (-30%) on 2025.

Drilling a little deeper, private housing construction-starts declined by 9% against the preceding three months and by 34% against the previous year. Social Housing starts were similarly depressed, dropping by roughly a quarter (-24%) against the preceding three months and by 16% against the previous year.

Sector Analysis – Non-Residential

According to Glenigan’s data, Offices were the only vertical to experience a growth spurt compared to the previous quarter, up 37%, to stand over two-thirds (+67%) above 2025 levels. This uptick in activity was primarily supported by the £50 million 105 Old Broad Street office development in the City of London.

The only other vertical to increase against the previous quarter was Retail, which rose 12% against the preceding three months. However, this modest leap wasn’t enough to bring it above last year’s results, falling 17% by comparison.

Hotel & Leisure and Education had a mixed period, with both falling by around a quarter (-25% and -24% respectively) compared to the previous quarter. However, both finished up when measured against last year, rising 1% and 23% respectively.

Elsewhere, performance plummeted. Industrial experienced an especially lacklustre period, nosediving by 36% against the preceding three months to stand 31% below the previous year.

Likewise, Health declined 16% against the preceding three months to stand 13% lower than the previous year. Community and Amenity project-starts, which have recently posted positive results are now in recession, falling by 37% against the preceding three months to stand 10% down against the previous year.

Sector Analysis – Civils

The bottom fell out of Civils, with work starting on-site cascading 37% against the preceding three months and falling 34% against the previous year.

Breaking it down, Infrastructure work starting on-site declined 32% against the preceding three months and declined by 37% on the previous year.

Similarly, Utilities declined 42% against the preceding three months and by 30% against the previous year.

The Regional Outlook

According to Glenigan’s regional data, the performance picture was inconsistent.

Once again, London was the stand out performer, experiencing a strong performance, rising 26% against the preceding three months to stand 69% up against the previous year. This was underpinned by a strong performance from the Office sector, which helped drive growth in the region.

It was more of a mixed bag for some of the regions. Northern Ireland experienced a mixed performance, dipping 2% against the preceding three months to finish 37% up against the previous year.

The North East performed similarly, dropping 27% against the preceding three months to stand 16% up compared to 2025 levels.

It was a less positive story for the remainder of the UK. Particularly in the South West where performance crashed, falling 47% against Q4 to stand 54% down against the previous year.

Not to be outdone in the disappointment stakes, the West Midlands also experienced a poor period, declining by 37% against the preceding three months to finish 39% lower than last year’s figures.

Finally, the South East performed poorly, declining 22% against the preceding three months to stand 27% down against the previous year.

Find out more about Glenigan here: www.glenigan.com

Building, Design & Construction Magazine | The Choice of Industry Professionals