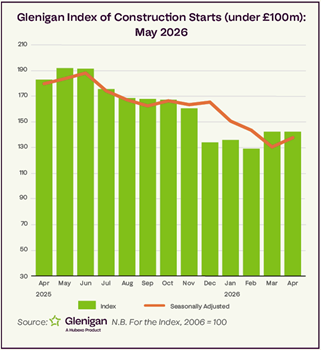

- The value of work starting on-site during the three months to April dropped 9% and remained 22% below 2025 levels.

- Residential construction starts declined 8% on the preceding three months and declined 33% against 2025 figures.

- Non-residential project-starts remained flat against the preceding three months to stand 2% up on a year ago.

Today, Glenigan releases the May 2026 edition of its Construction Index.

The Index focuses on the three months to the end of April 2026, covering all underlying projects, with a total value of £100 million or less (unless otherwise indicated), with all figures seasonally adjusted.

It’s a report which provides a detailed and comprehensive analysis of year-on-year construction data, giving built environment professionals a unique insight into sector performance over the last 12 months.

The May edition continues the general theme of sector-wide decline, as the US-Iran War drags on, disrupting international supply chains.

Overall, the value of work starting on site in the three months to April fell by 9% and finished a fifth (-22%) below 2025 levels.

Whilst the fall is less severe than seen during previous months, there’s a general fear that the industry is within the eye of the storm and these results are a harbinger of potentially worse to come, as the supply chain disruption really hits home. Aside from international turmoil, political in-fighting on the home front has led to policy stagnation and a lack of investor and consumer confidence means contractors and subcontractors are keeping their shovels clean until greater certainty returns.

Commenting on the Index, Glenigan’s Economics Director, Allan Wilen said, “Construction markets are becalmed. Faced with heighted geopolitical uncertainty generated by the Iran War, investors are reassessing their development plans. Whilst a rise in office, retail and health projects helped stabilise non-residential starts during the three months to April, both residential and civil engineering starts continued to decline. Parliament has now been prorogued and hopefully the King’s Speech, which comes after a successful State Visit to the United States, will provide an opportunity to reassess and reset the national direction.”

He cautions, “However, whatever the outcome of the coming weeks, there’s a general consensus that there will be fewer opportunities in the back half of this year, which also implies far fiercer competition. Savvy players will no doubt have strategies in place to capitalise on this risk and opportunity, and I’d urge those who are currently behind the curve to start seriously considering their own game plans and how they can stay afloat during an upcoming period of disruption. Niches, including data centres, purpose-built student accommodation and supermarkets, present pockets of growth and those than can either already service or diversify to meet requirements stand to weather the headwinds currently gathering force.”

Taking a closer look at individual sectors and verticals…

Sector Analysis – Residential

Residential construction remains stuck in a downward spiral as buyers hesitate and demand continues to stagnate. Developers face massive economic pressures, coupled with steep regulatory hurdles and planning headaches, stifling activity.

Glenigan’s data revealed that starts declined 8% during the Index period, falling a third

(-33%) against 2025 figures.

Drilling deeper, private starts plummeted 39% compared to last year, dropping 9% on the preceding three months. The fall for social housing was slightly less severe, dipping 4% against the previous three months and it fell 16% on last year.

Sector Analysis – Non-Residential

There were a few bright spots within the non-residential verticals which posted a relatively modest increase of 2% against the previous year and remained flat during the Index period.

This slight uptick was predominantly driven by offices, which experienced an exceptionally strong period, rocketing 99% over the preceding three months and remaining an impressive 94% above 2025 results.

According to Glenigan, this was largely driven by activity in the capital, with standout projects like the £50 million 105 Old Broad Street office refurbishment in the City of London contributing to growth.

In other verticals it was a mixed bag. Encouragingly, retail increased 13% against the preceding three months, but this renewed momentum failed to make up for lost ground on 2025 levels (-9%). Likewise, health rose 12% compared to the previous three months but faltered compared to last year’s figures (-10%). Conversely, education fell 10% during the Index period but finished 12% up on 2025 results.

Unfortunately, all other verticals saw substantial decline as the geopolitical turmoil started to really bite, disrupting vital supply chains, driving up costs and dampening confidence, inevitably leading to delays.

As Glenigan’s data show, this was most acutely seen within civils where work starting on-site crashed, tumbling 42% against the preceding three months and seeing performance slashed almost in half (-47%) compared to the previous year. Diving into the detail, Infrastructure work starting on-site fell 19% against the preceding three months and declined by 48% on last year. Utilities fared even worse, nosediving 56% against the preceding three months and by 46% against 2025 levels.

Community and amenity project-starts also registered a particularly poor period, cascading by over a third (-39%) during the Index period to stand 45% down on the previous year.

Slightly less severe, yet still disappointing, Hotel & Leisure activity stumbled, having declined 32% against the preceding three months to stand 17% down against the previous year. Similarly, Industrial fared no better, falling 23% against the preceding three months, finishing 29% below the previous year.

Regional Outlook

Regionally, there were a handful of outliers with London experiencing a particularly robust Index period, soaring 25% against the preceding three months to finish 59% up on 2025 results. As previously noted, a strong performance in the office sector helped drive this growth.

Northern Ireland was also in clover, rising 20% compared to the preceding three months to stand 53% up on the previous year. More modestly, yet no less impressive, the North East also performed well, posting a 14% increase during the Index period, up by almost a fifth against the previous year.

Elsewhere, the picture painted was one of decline. The West Midlands experienced an especially poor period, declining 17% against the preceding three months and declining 36% against the previous year.

The South West also performed poorly, declining 44% against the preceding three months to stand a dismal 60% down against the previous year. Not to be outdone, the South East also declined, by 17% against the preceding three months and by 34% against the previous year.

Find out more about Glenigan here: www.glenigan.com

Building, Design & Construction Magazine | The Choice of Industry Professionals