Glenigan Review reveals choked activity as international conflict strangles pipeline

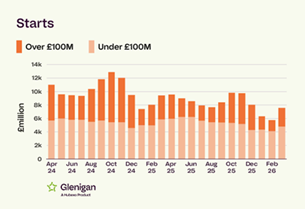

- Starts on-site see value fall by 6% compared to the previous three months, finishing 20% lower than 2025 levels

- Main contract awards increased by 3% against last year’s figures, up by 30% against the preceding three months

- Detailed planning approvals experience a 29% reduction in value over the Review period, plummeting by 51% on the previous year’s performance

Today, Glenigan | A Hubexo Company (Glenigan), one of the construction industry’s leading insight and intelligence experts, releases the April 2026 edition of its Construction Review.

The Review focuses on the three months to the end of March 2026, covering all major (>£100m) and underlying (<£100m) projects, with all underlying figures seasonally adjusted.

It’s a report providing a detailed and comprehensive analysis of year-on-year construction data, giving built environment professionals a unique insight into sector performance over the past year.

The April Review paints a bleak picture of an industry buffeted by frustratingly persistent socioeconomic headwinds.

The poor project starts figures, recorded in the three months to the end of March 2026, fell back 6%, whilst nosediving by 20% on 2025 levels.

Glenigan’s data shows activity becoming increasingly uneven sector-wide and, whilst main contract awards rose against the preceding quarter (+30%) and last year (+3%), fewer projects are actually making it to site. As such, these positive results ring hollow.

This cooling-off is acutely observed in a significant decline in detailed planning approvals, which saw their value slashed in half (-51%) compared to 2025 levels, falling by almost a third (-29%) during the review period.

Global markets are in a state of shock, prompted by the escalation of the US/Iran war, which has led to the closure of key trading routes, damaging investor confidence. This is likely to exacerbate the current downward spiral over the coming months.

Commenting on the April Review, Allan Wilen, Glenigan’s Economics Director, says, “Private investment and consumer spend has stalled. A general increase in the cost of living is squeezing household spending and denting homebuyers’ confidence, while investors are cautious given the weak economic outlook, stifling potential momentum in the property market and resulting in general wariness. The Iran War is exacerbating these pressures by stoking inflation and further weakening economic growth. Unfortunately, this situation is unlikely to end in the near term, with energy costs expected to remain high this year and the prospect of interest rates cuts fading fast.

“This growing culture of cautiousness is extending to contractors, subcontractors and product manufacturers alike, where higher oil prices are starting to cascade down the supply chain, raising energy, material, transport and on-site costs. Already battling against uncomfortable financial conditions, skills shortages and a deluge of complex regulations, it’s little wonder that many are keeping their powder dry until economic stability returns.”

Drilling down into the sector verticals, performance was inconsistent, in line with the overall findings of the April Review. Despite remaining well behind the preceding quarter’s results, there were a few indicators that show, when measured against 2025 levels, activity hasn’t completely ground to a halt and the pipeline flow, whilst weak, is still active.

Taking a closer look…

Strong starts

According to Glenigan data, Offices, Hotel & Leisure and Education stood out during the quarter, registering strong year-on-year growth in project starts. Offices led the way with a 75% surge, while Hotel & Leisure and Education both posted 31% increases, a broadly positive picture against a backdrop of wider market uncertainty. That said, forward-looking indicators were more cautious across Office and Hotel & Leisure, with main contract awards and detailed planning approvals declining year-on-year in each case, suggesting the pipeline may soften in the months ahead.

Within Offices, growth was broad-based, with the value of major projects rising by 84% year-on-year. Data centre construction has been a key driver, though the sector faces headwinds from rising industrial electricity costs and grid-connection delays, illustrated by the indefinite pause on OpenAI’s Stargate UK scheme in North Tyneside. In Hotel & Leisure, indoor leisure facilities and cinemas and theatres were the standout performers, rising 133% and 186% respectively, while hotels and guest houses fell 30%. Education continued to benefit from the Schools Rebuilding Programme, with schools dominating activity and university schemes contributing meaningfully, though college projects declined.

Regionally, London dominated Office activity with starts up by 124% year-on-year, boosted by a major data centre scheme. The South West surged 15-fold. In Hotel & Leisure, Scotland led with a 205% rise, closely followed by London and the South West, which quadrupled year-on-year. Education starts were also strongest in London, with Scotland also making a solid contribution driven by public-sector investment.

It’s a deal

Two sectors registered a rise in main contract awards against 2025 levels during the quarter: Housing and Civil Engineering. Housing delivered a 41% increase year-on-year, while Civils posted an 11% rise, encouraging signals for future workloads in both sectors. The picture was more complex beneath the surface, however, with project starts declining in both cases and planning approvals remaining under pressure, particularly in Civils where approvals fell 81% year-on-year.

In Housing, the uplift in starts was driven largely by major projects, with social sector housing the dominant force, up 230% year-on-year and accounting for 41% of all starts. Private housing and private apartments, by contrast, fell 44% and 50% respectively. The outlook is cautiously optimistic but fragile, with global instability and early signs of softening house prices (including a decline reported by Halifax) suggesting the recovery may be short-lived. In Civils, energy schemes remained a significant component despite falling below last year’s levels. Airport-related infrastructure recorded growth, albeit from a low base, and future investment in road, rail and utilities infrastructure is expected to provide a firmer foundation from 2026/27.

Regionally, Yorkshire & the Humber dominated housing project starts, substantially driven by major social housing heating works in Leeds, while London was the second most active region, despite a moderate decline. In Civils, London led project starts, rising 143%, while Scotland accounted for the largest share of planning approvals at 20%, though activity there fell 39% year-on-year. Northern Ireland recorded sharp approval growth of 903%, pointing to potential future activity in the region.

Seal of approval

Glenigan’s data highlights that Health, Retail and Community & Amenity shared a common thread during the quarter: while project starts and main contract awards declined year-on-year across all three, detailed planning approvals rose in each case, pointing to a strengthening development pipeline and reasons for cautious optimism further out. Health approvals rose 8%, Retail climbed 21% and Community & Amenity grew 14%, a consistent signal that activity may pick up in the quarters ahead, even if near-term construction output remains subdued.

In Health, hospitals accounted for the largest share of starts but at substantially lower values than the previous year, with growth coming instead from smaller-scale dental, health and veterinary centres and day centres. The New Hospital Programme, proposed NHS technology investment and increased Budget funding for routine spending all point to a gradual recovery. In Retail, supermarkets dominated activity, accounting for 75% of starts and growing 17% year-on-year, while shops fell 50% and petrol stations edged down 4%. Supply chain disruptions and geopolitical instability remain headwinds for the sector. In Community & Amenity, government buildings were the standout, rising 532% year-on-year and accounting for 60% of starts, while blue light projects grew 31%.

Regionally, the South East led Health project starts with a 26% share, supported by the New Wycombe Hospital, while Wales and Scotland both recorded notable year-on-year growth. In Retail, the South East topped starts with a 39% rise, with the North East posting the strongest growth at 93%. The North West was the most active region for Community & Amenity starts with a 219% rise, closely followed by the North East, which jumped more than tenfold year-on-year.

Building, Design & Construction Magazine | The Choice of Industry Professionals