City centre development is becoming more integrated, with residential rental tenures now dominating delivery, prime office supply tightening, and retail reshaping regeneration across the UK’s major regional cities, according to a new report by Savills.

This new phase of regeneration within UK cities is becoming defined by increasingly integrated mixed-use development, as residential, commercial and leisure uses become more interdependent in response to shifting economic dynamics, changing patterns of urban living and evolving investor preferences.

Across regional markets, the balance between demand, development viability and structural change is shaping the next cycle of urban growth.

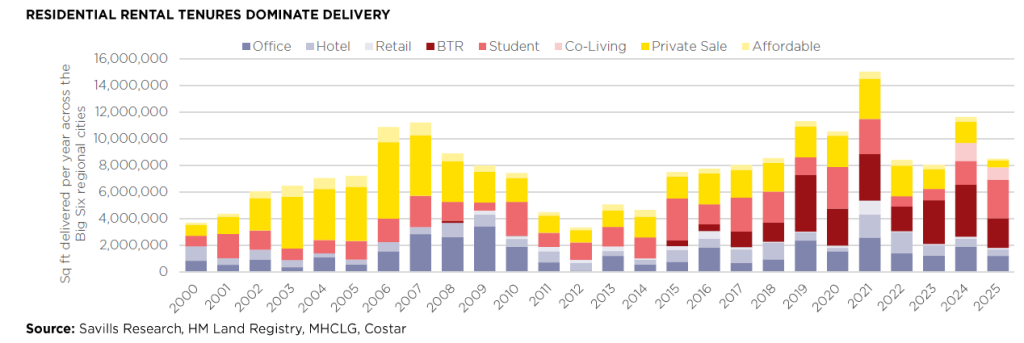

According to the latest report by Savills Research – UK Cities: a mixed-use perspective – the decade leading up to the global financial crisis saw city centre development in the Big Six regional cities (Birmingham, Bristol, Edinburgh, Glasgow, Leeds and Manchester) dominated by private sale housing. Over the last 10 years, however, a much broader mix of uses has emerged, with Build to Rent (BTR) overtaking private sale as the primary driver of city centre housing delivery, Purpose-Built Student Accommodation (PBSA) expanding rapidly, and co-living emerging as a new asset class.

This shift reflects strong demand fundamentals and the growing role of institutional capital, which has supported large scale, placemaking-led regeneration. Savills notes that rental growth across the Big Six has averaged between 4% and 7.5% per year over the last five years, supporting strong returns – although continued build cost increases and growing affordability pressures mean developers and local planning authorities will need to take a pragmatic approach to viability in order to maintain strong development pipelines.

The report also highlights a significant structural shift in office markets. In the post-pandemic environment, uncertainty around hybrid working contributed to rising vacancy in older, less efficient buildings, but demand has become increasingly polarised as occupiers prioritise modern, highly sustainable offices in central, well-connected locations. More than 60% of expected 2026 office take-up is forecast to be Grade A and prime, underlining the depth of demand for high-quality space.

At the same time, the office development pipeline remains exceptionally thin. Savills states that only Manchester and Leeds currently have new schemes under construction that are due to complete beyond 2026, leaving supply constrained just as occupiers focus on securing prime accommodation. Prime headline office rents have risen by an average of 30% over the past five years and, if that trajectory continues, could soon approach the £60 per sq. ft. threshold that many developers consider necessary to re-establish viability.

Retail is also evolving, moving away from traditional formats towards mixed-use environments centred on experience, leisure, and food and beverage. In this context, retail plays an essential role in placemaking by supporting footfall and enhancing the attractiveness of city centres. Ground-floor activation – including shops, bars, restaurants and cafés – is increasingly recognised as the element that connects homes, offices and hotels, helping to attract target occupiers and residents while maximising value across the wider scheme.

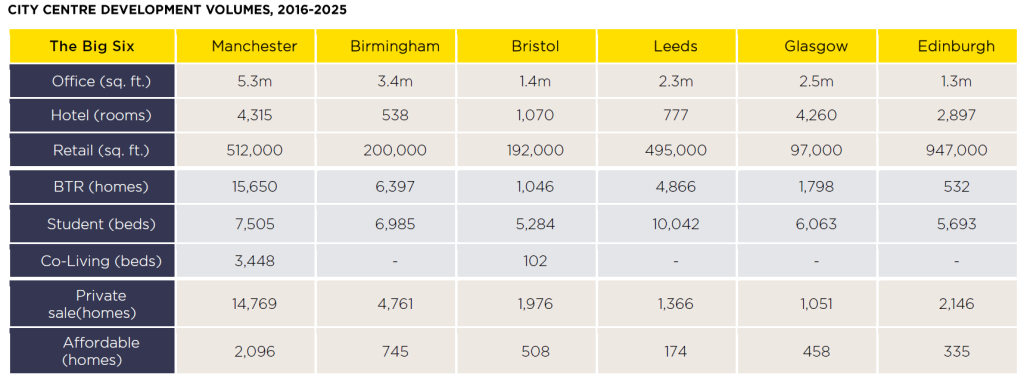

Research from Savills also illustrates the scale and diversity of delivery across the UK’s major urban markets between 2016-2025. Among the Big Six, Manchester recorded 5.3 million sq. ft. of office delivery, 15,650 BTR homes and 3,448 co-living beds, while Birmingham delivered 3.4 million sq. ft. of offices, 6,397 BTR homes and 6,985 student beds. Leeds delivered 10,042 student beds, while Edinburgh recorded 947,000 sq. ft. of retail delivery.

Looking ahead, Savills says city centre development will continue to be driven by strong underlying demand, but increasingly constrained by viability challenges.

Emily Williams, Director of Residential Research at Savills, says: “Residential is expected to remain at the heart of city centre regeneration, particularly through rental-led models, although rental growth is expected to moderate as affordability limits are reached. High construction costs, borrowing costs and regulation are all expected to continue restricting new supply and widening the gap between demand and delivery.”

Jonathan Lambert, Co-lead of Savills’ Mixed-Use Sector Group, adds: “Market polarisation is certainly a defining theme, with larger and more established cities best placed to sustain development, while smaller or more constrained markets may struggle in a higher-cost, higher-risk environment, particularly where planning obligations present too many challenges.

“Local authorities will need to adopt a pragmatic approach to viability, with public-private partnerships and the attraction of long-term patient institutional capital likely to be key to unlocking future opportunities.”

Building, Design & Construction Magazine | The Choice of Industry Professionals